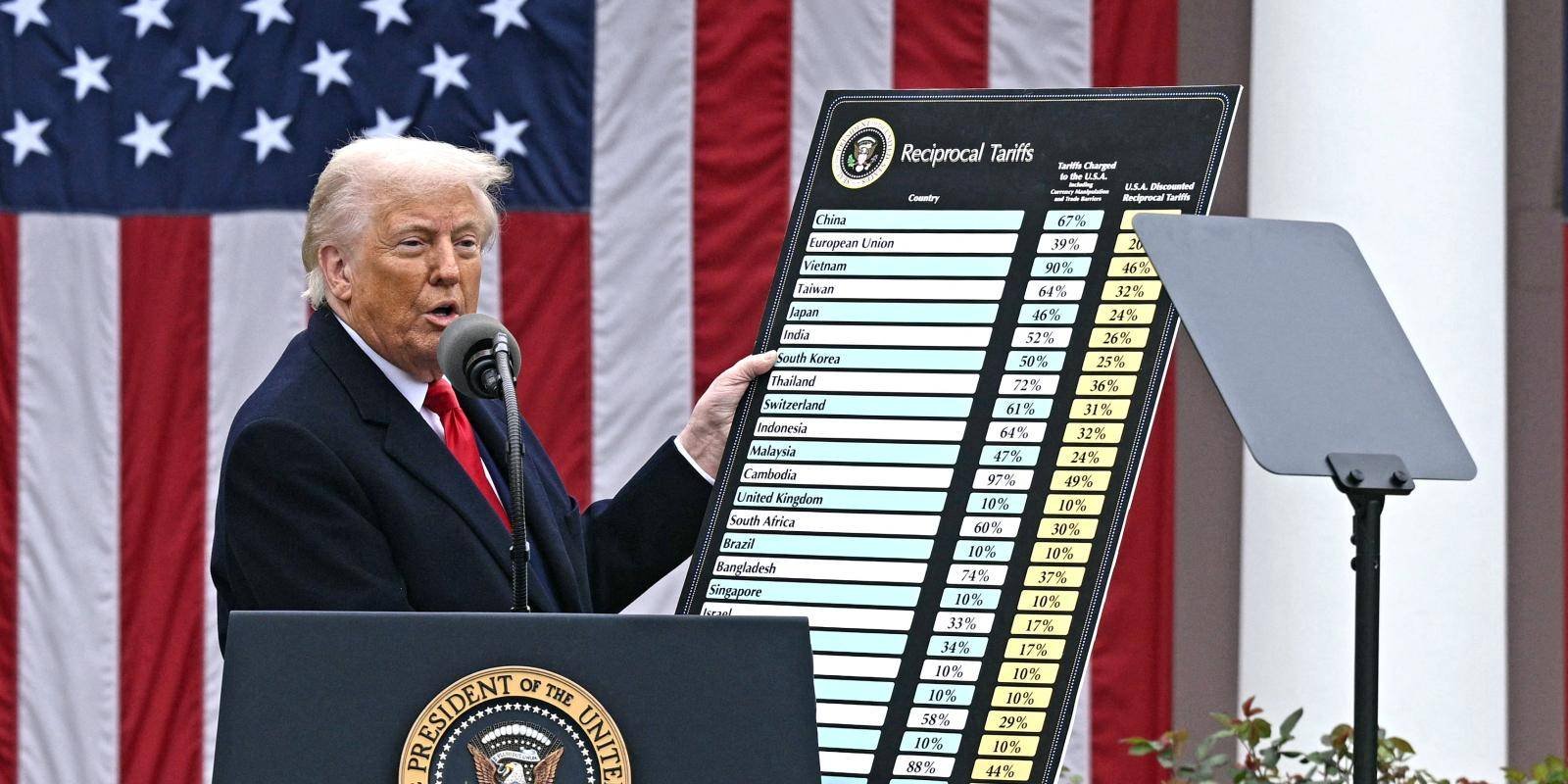

The recent Supreme Court ruling invalidating President Trump’s broad import tariffs marks a turning point in U.S. trade policy. By declaring these tariffs unconstitutional under the International Emergency Economic Powers Act, the Court reaffirmed that sweeping trade measures require explicit Congressional authority. For businesses, this decision is more than a legal milestone; it presents both immediate relief and a framework for strategic foresight.

Firms that previously faced inflated costs from tariffs can anticipate lower input prices, particularly in sectors dependent on imported raw materials such as manufacturing, construction, and electronics. Businesses awaiting refunds will need to manage cash flow carefully, as reimbursement processes may be slow and uneven. Smaller firms, in particular, must plan liquidity contingencies to bridge the gap until refunds are processed.

Beyond immediate cost relief, the ruling highlights the importance of monitoring policy uncertainty. While these tariffs are struck down, the administration may explore alternative statutory mechanisms to reintroduce import duties. Businesses must therefore adopt dynamic risk assessment, modeling potential policy shifts and building flexibility into procurement, pricing, and inventory strategies.

The broader economic lesson is clear: tariffs rarely achieve intended objectives without substantial cost to domestic businesses and consumers. In past years, U.S. firms absorbed most of the financial burden, either through higher input costs or price adjustments for consumers. Companies that anticipate shifts in trade policy can gain competitive advantage by diversifying supply chains, identifying alternative sourcing, and optimizing operational efficiency before competitors react.

Strategically, the ruling offers a window for businesses to recalibrate. Firms can re-evaluate contracts, renegotiate supplier terms, and plan investments with a clearer expectation of costs. Importers can consider long-term agreements while monitoring potential new tariff routes. The key takeaway is that foresight and preparedness in the face of regulatory unpredictability is critical; organizations that proactively model scenarios are better positioned to maintain margins, respond to market shifts, and seize opportunities arising from competitors’ hesitation.

In conclusion, while the Supreme Court decision mitigates immediate tariff pressures, it also underscores that trade policy remains volatile. Businesses that understand both the direct financial impact and the broader policy landscape can leverage this clarity to strengthen operations, reduce risk, and maintain strategic agility. Those who integrate foresight into planning will turn uncertainty into opportunity, navigating a complex trade environment more effectively than reactive competitors.