29 April 2026

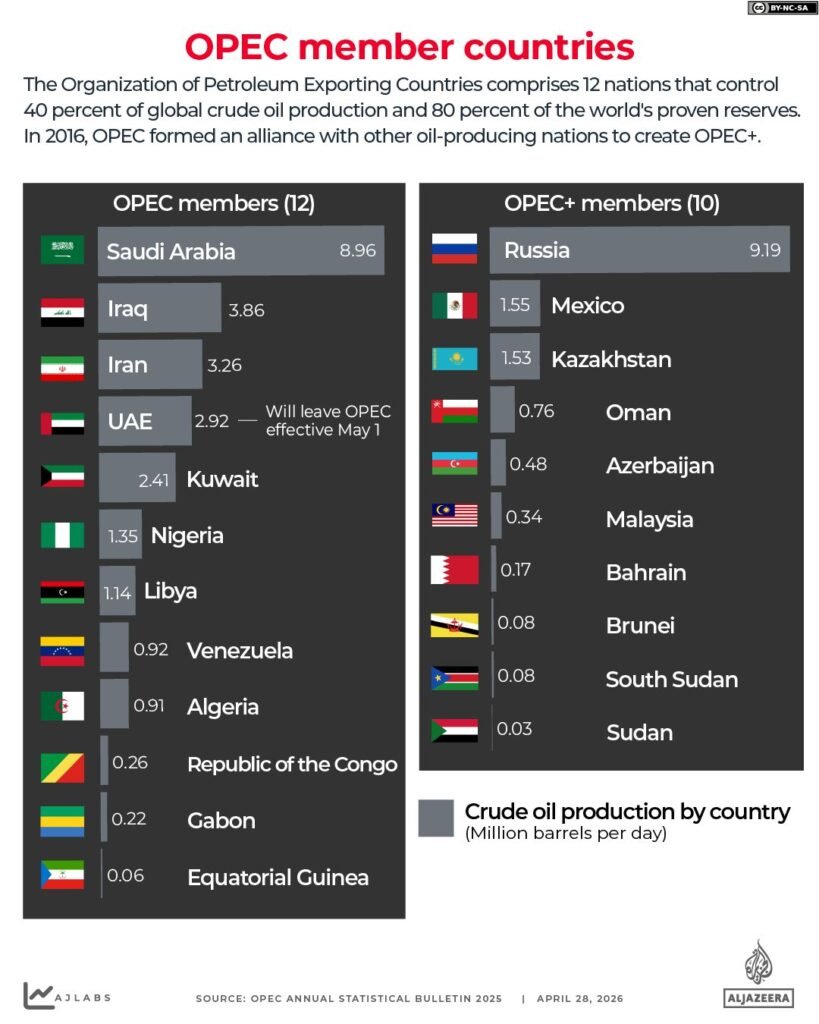

The decision by the Organization of the Petroleum Exporting Countries to lose one of its key members, the United Arab Emirates, marks a pivotal moment in global energy markets. After more than 50 years in the oil producers’ alliance, the UAE has announced its withdrawal effective May 2026, a move driven largely by economic considerations rather than purely political motives. The development reflects changing priorities within oil-exporting nations and highlights deeper structural shifts in the global oil economy.

Economically, the UAE’s exit is closely tied to its ambition to expand oil production capacity and maximize export revenues. As one of OPEC’s top producers, the country has been producing around 3 to 3.5 million barrels per day under quota limits. However, its national oil company, Abu Dhabi National Oil Company, has invested heavily in upstream infrastructure with the goal of increasing capacity to approximately 5 million barrels per day in the coming years. Remaining within OPEC would have required adherence to production ceilings, limiting the country’s ability to fully capitalize on its investments.

At a time when global oil prices have remained elevated frequently trading above $100 per barrel amid geopolitical instability the ability to independently increase output offers a clear economic advantage. Higher production levels allow the UAE to boost export volumes and government revenues, which remain closely tied to hydrocarbons despite ongoing diversification efforts. Oil and gas still contribute roughly 30% of the UAE’s GDP and a significant share of fiscal income, making production policy a central economic lever.

The departure also weakens OPEC’s overall influence in the global oil market. Historically, the organization has controlled a substantial share of global supply, enabling it to stabilize prices through coordinated output adjustments. However, its share has gradually declined in recent years, falling from about 48% to around 44% of global supply in early 2026. The exit of a major producer like the UAE further reduces the group’s ability to enforce collective discipline and manage price levels effectively.

This erosion of market control has broader economic implications. Without coordinated production targets, oil markets may become more competitive but also more volatile. Countries acting independently could increase supply during periods of high prices, potentially pushing prices downward over time. For oil-importing economies, this could provide relief through lower energy costs and reduced inflationary pressures. On the other hand, greater volatility complicates investment planning for both producers and consumers, as price swings become more pronounced in response to geopolitical or demand shocks.

In the short term, the UAE’s exit is unlikely to cause immediate disruption to oil prices due to existing global uncertainties. Tensions in key transit routes such as the Strait of Hormuz, through which nearly 20% of global oil trade passes, have already contributed to tight supply conditions. As a result, market reactions to the announcement have been relatively muted, with only brief price fluctuations observed following the news.

Over the longer term, however, the shift could contribute to a gradual transformation of global oil dynamics. Increased production from non-OPEC or former OPEC members may lead to a more decentralized supply structure. This would mark a departure from decades of cartel-driven market management toward a system influenced more by market competition and national strategies.

The UAE’s move also aligns with its broader economic diversification agenda. While expanding oil production in the near term, the country continues to invest in renewable energy, nuclear power, and non-oil sectors such as finance, tourism, and technology. This dual strategy allows the UAE to maximize current hydrocarbon revenues while preparing for a future less dependent on fossil fuels. Notably, nuclear energy already contributes about a quarter of the country’s electricity generation, reflecting a significant shift in its domestic energy mix.

Financial markets have reacted cautiously to the development, with analysts noting both risks and opportunities. Some estimates suggest that increased independent production could place downward pressure on oil prices over time, while others emphasize the likelihood of increased price swings. In early trading following the announcement, oil prices experienced intraday movements of up to 3%, underscoring market uncertainty about the long-term impact.

Ultimately, the UAE’s departure from OPEC underscores a growing tension between collective market management and national economic priorities. By prioritizing production flexibility and revenue maximization, the UAE is betting on its ability to compete effectively in a more open market environment. The decision may encourage other producers to reassess their positions within the cartel, potentially accelerating a broader shift in how global oil markets are structured.

As the global economy continues to navigate energy transition pressures, geopolitical risks, and fluctuating demand patterns, the UAE’s exit represents more than a single policy change. It signals a rebalancing of power within the oil industry and raises important questions about the future role of OPEC in shaping global energy economics.